Navigating the landscape of UK commercial finance can feel like a minefield, especially when your legal structure dictates your borrowing power. Whether you are a freelance consultant or a director of a scaling enterprise, securing business loans for sole traders and limited companies is often the catalyst for the next stage of your growth. However, the path to approval looks very different depending on how your business is registered with Companies House or HMRC.

Many business owners find themselves at a crossroads: does being a sole trader limit my access to capital? Or does a limited company structure provide a “shield” that makes lenders more comfortable? In this guide, we break down the complex world of SME lending to ensure you find the perfect financial fit for your specific needs.

At Pello Pay, we believe in a “human + tech” approach. While some platforms rely solely on algorithms, we combine cutting-edge technology with expert human intuition to ensure you aren’t just getting a “fast” loan, but the right loan.

Table of Contents

1. Understanding the Core Differences: Sole Trader vs. Limited Company

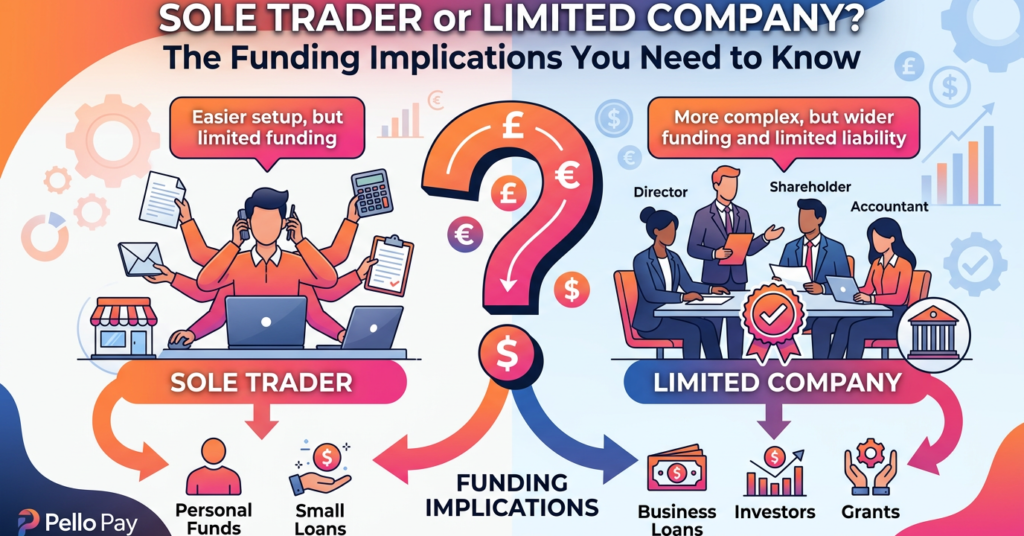

Before diving into business loans for sole traders and limited companies, it is vital to understand why lenders view these entities differently. A sole trader is the “alter ego” of the individual. Legally, there is no distinction between the business owner and the business itself.

Conversely, a limited company is a separate legal entity. It has its own assets, its own debts, and its own credit profile. This distinction is the foundation upon which all UK lending decisions are built. While a sole trader might find it easier to set up, a limited company often finds it easier to separate personal risk from professional growth.

2. Liability and Risk: How It Affects Your Borrowing Power

Risk is the primary language of lenders. When assessing applications for business loans for sole traders and limited companies, underwriters look at who is ultimately responsible for the debt.

For sole traders, the “unlimited liability” means your personal assets—including your home—could be at risk if the business fails to meet its repayments. While this sounds daunting, it actually provides a level of security to the lender, sometimes leading to faster approvals for smaller amounts.

For limited companies, the “limited liability” protects the directors’ personal assets. However, for many small and medium-sized enterprises (SMEs), lenders will still require a “Personal Guarantee” (PG). This effectively bridges the gap, ensuring that the human behind the tech is committed to the loan’s success.

According to recent data from UK Finance, the demand for flexible SME lending has shifted significantly toward unsecured options that don’t require heavy collateral but do rely on strong trading history.

3. Business Loans for Sole Traders: The Personal Credit Factor

If you are operating as a sole trader, your personal credit score is the star of the show. Because you and the business are one and the same, lenders will scrutinize your personal financial habits.

Key benefits of sole trader funding include:

- Simplicity: Fewer legal documents are required compared to a limited company.

- Speed: Ideal for Short Term Loans to cover immediate cash flow gaps.

- Flexibility: You have total control over how the funds are deployed without needing board resolutions.

However, the challenge lies in the “ceiling” of funding. Many high-street banks are hesitant to lend large sums to sole traders without significant security. This is where a modern platform like Pello Pay excels, looking beyond the credit score to the actual health of your daily cash flow.

4. Business Loans for Limited Companies: Building Corporate Credit

For limited companies, the focus shifts to the company’s balance sheet. Lenders want to see profitability, consistent turnover, and a healthy “Current Ratio” (assets vs. liabilities).

Advantages for Limited Companies:

- Higher Loan Amounts: Access to larger Long Term Loans for major expansions.

- Corporate Credibility: A limited company structure is often a prerequisite for complex finance like Invoice Finance.

- Tax Efficiency: Interest payments on business loans are generally tax-deductible as a business expense.

Building a strong corporate credit score takes time. For newer companies, Pello Pay offers “Smart Funding Advice” to help you position your business in the best light for underwriters, rather than just relying on an automated “Yes/No” algorithm.

5. Types of Flexible Business Finance Available

The “one-size-fits-all” approach to banking is dead. Today’s business owners need a suite of products that react to the market. When searching for business loans for sole traders and limited companies, consider these specialized options:

- Working Capital Loans: Designed for the day-to-day “rhythm” of your business.

- Merchant Cash Advances: Perfect for retail or hospitality businesses that take card payments.

- Bridging Loans: Short-term “gap” funding while waiting for a larger capital event.

- Revolving Credit Lines: Draw down what you need, when you need it.

If your business is facing an unexpected crisis or a sudden opportunity, exploring our Emergency Loans can provide the liquidity needed within hours, not weeks.

6. Asset Finance: Unlocking Growth for All Structures

Whether you are a sole trader or a limited company, you likely need equipment to operate. From vehicles to heavy machinery or high-end IT hardware, buying these outright can cripple your cash flow.

Asset Finance allows you to spread the cost of the equipment over its useful life. The asset itself often serves as the security for the loan, which can make this an easier route for sole traders who don’t want to put their personal property at risk.

At Pello Pay, our Asset Finance specialists understand that a piece of machinery isn’t just a cost—it’s a revenue generator. We help you calculate the ROI of your purchase to ensure the finance pays for itself.

7. Unsecured vs. Secured Loans: What You Need to Know

This is the most common question we receive regarding business loans for sole traders and limited companies.

- Unsecured Loans: No physical collateral is required. These are typically based on your business’s revenue and creditworthiness. They are faster to process but may carry slightly higher interest rates. Check our Unsecured Loans for more details.

- Secured Loans: These require an asset (like property or inventory) to be used as security. These are often used for larger sums and offer lower interest rates and longer repayment terms. For major investments, see our Secured Loans page.

8. Application Checklist: Documents Required

To ensure your application for business loans for sole traders and limited companies moves through the “tech” phase and into the “human” review phase quickly, have these documents ready:

- For Sole Traders: 3-6 months of personal and business bank statements, and your latest SA302 from HMRC.

- For Limited Companies: 6 months of business bank statements, latest filed accounts (full or abridged), and a summary of current business debt.

- For Both: Identification (Passport/Driving License) and proof of address.

9. The Pello Pay Advantage: Beyond the 90-Second Match

Our competitor, Fund Onion, focuses heavily on the “AI speed” of a 90-second match. While we utilize similar high-speed technology to scan the market, we believe that speed without strategy is a risk.

Why Pello Pay is different:

- Human Oversight: Every application is looked at by a person who understands the nuances of UK industries.

- Product Breadth: We don’t just offer “standard” loans; we provide everything from invoice factoring to complex asset restructuring.

- Growth Focus: We aren’t just here for a one-off transaction. We want to be your long-term finance partner.

If you are unsure which structure suits your current growth trajectory, speak to a Pello Pay broker today for a no-obligation consultation.

10. Conclusion: Choosing the Right Path

The choice between business loans for sole traders and limited companies isn’t about which is “better,” but which is “better for right now.” Sole traders enjoy speed and simplicity, while limited companies benefit from scalability and risk mitigation.

Regardless of your structure, the UK finance market is currently favoring businesses that show resilience and a clear plan for growth. As interest rates fluctuate—keep an eye on the latest Bank of England Base Rate—having a flexible finance partner is more important than ever.

Ready to take the next step? Whether you need to bridge a cash flow gap or invest in new machinery, Pello Pay is here to help you navigate the journey.

Explore our Business Loans today or Refer a Business to our network and help another SME grow.